Graduation के बाद Student Loan की EMI कब और कैसे शुरू होती है? जो बैंक नहीं बताता — वो सब यहाँ जानिए!

Every year lakhs of Indian graduates are blindsided by education loan repayment — because banks explain the process poorly. From moratorium period tricks to interest capitalisation, EMI calculation, tax benefits under Section 80E, and what to do if you can't pay — this complete guide covers everything you must know before your first EMI arrives!

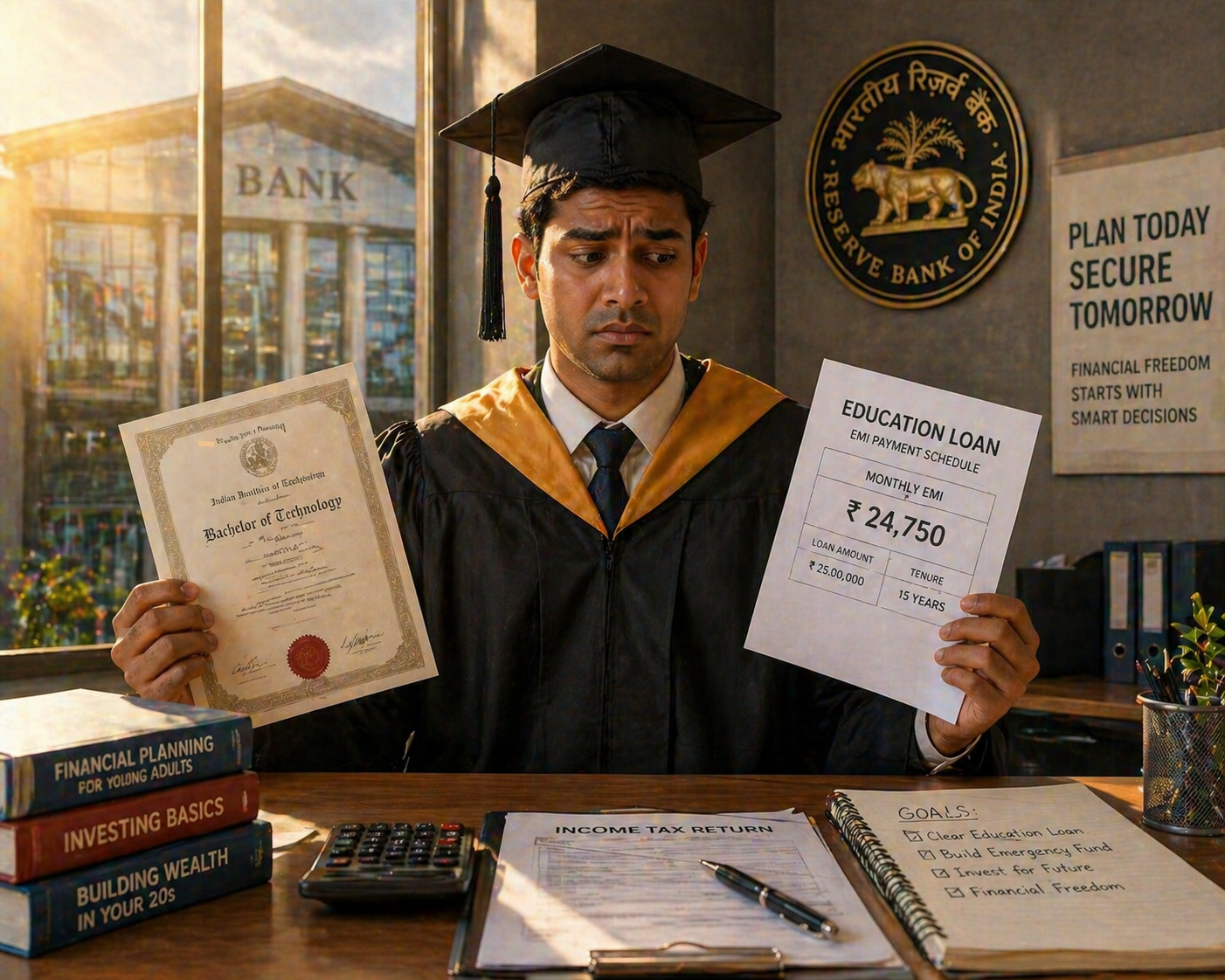

Graduation के बाद Student Loan — जो कोई नहीं बताता, वो आज जान लो

Degree मिली, खुशी मनाई — और फिर inbox में आया पहला loan repayment reminder। यही है लाखों Indian graduates की reality। हर साल lakhs of students education loan लेकर पढ़ाई पूरी करते हैं, लेकिन repayment कैसे शुरू होती है — यह उन्हें ठीक से कोई नहीं समझाता। न बैंक, न कोई और। आज इस पूरी process को step-by-step समझते हैं — ताकि पहली EMI से पहले आप पूरी तरह तैयार हों।

Moratorium Period — आपका "Buffer Window" क्या है?

हर education loan India में एक moratorium period के साथ आता है। यह वह grace window है जो course खत्म होने और EMI शुरू होने के बीच होती है।

RBI के guidelines के अनुसार structure:

Course complete होने के बाद 6 महीने से 1 साल तक moratorium मिलता है

या job मिलने के 6 महीने बाद — जो भी पहले हो

SBI, Bank of Baroda, Punjab National Bank जैसे public sector banks यही standard structure follow करते हैं।

लेकिन यहाँ एक बड़ा catch है जो ज़्यादातर students को नहीं पता:

Moratorium में EMI नहीं देनी — लेकिन interest रुकता नहीं। Loan चुपचाप background में बढ़ता रहता है। यह interest आपके principal में add हो जाता है — इसे "Capitalisation of Interest" कहते हैं।

मतलब — जब आपकी पहली EMI due होगी, तब आप original amount से ज़्यादा के borrower होंगे।

Real Example — कितना बढ़ जाता है Loan?

मान लीजिए आपने ₹10 लाख 8.5% annual rate पर लिया।

एक साल के moratorium में लगभग ₹85,000 interest accumulate होता है।

अब आपकी EMI ₹10 लाख पर नहीं, ₹10.85 लाख पर calculate होगी।

8.5% rate पर 10 साल के tenure में यह difference आपकी monthly EMI में ₹500 extra जोड़ता है। 120 months में यह बनता है ₹60,000 extra — सिर्फ इसलिए कि moratorium में interest compound होता रहा।

Smart Move: अगर moratorium के दौरान कोई part-time job या freelance income हो — तो कम से कम interest portion का payment करते रहें। यह long-term में बड़ा फर्क डालता है।

EMI Calculate कैसे होती है? — पूरा Formula

Moratorium खत्म होने के बाद lender आपकी EMI calculate करता है — total outstanding amount पर जिसमें capitalised interest भी शामिल है।

Repayment tenure:

Loan amount और bank के terms के हिसाब से 5 से 15 साल तक

EMI के 3 factors:

Principal — original loan + capitalised interest

Interest Rate — fixed या floating

Tenure — जितना लंबा, EMI कम लेकिन total interest ज़्यादा

Pro Tip: अपने bank के IFSC code और loan account details तुरंत save करें। Auto-debit set up करें EMI due date से कम से कम 2 महीने पहले। Account में हमेशा 2 महीने की EMI buffer रखें।

अगर Job न मिले या EMI Pay न कर सकें — क्या करें?

Graduation के बाद हर किसी को 6 महीने में job नहीं मिलती। Salary expectations और reality में gap होता है। ऐसे में सबसे बड़ी गलती है — loan को ignore करना।

सही रास्ता क्या है?

तुरंत अपने bank से contact करें और repayment restructuring request करें। Banks legal recovery से ज़्यादा restructuring prefer करते हैं — क्योंकि legal process उनके लिए भी slow और expensive है।

क्या options मिल सकते हैं:

Longer tenure — EMI कम होगी, लेकिन total interest ज़्यादा देना होगा

Temporary EMI reduction — शुरुआती सालों में कम EMI का option

Step-up EMI — पहले कम, बाद में career grow होने पर ज़्यादा

Default करने के नतीजे — बहुत गंभीर हैं

Education loan default को कभी हल्के में न लें:

90 दिन बिना payment के — bank credit bureaus को default report कर देता है।

CIBIL Score seriously hit होती है — future में home loan, car loan, credit card सब मुश्किल हो जाता है।

Guarantor की liability — अगर आपने किसी को guarantor बनाया है तो उनकी भी financial life affected होगी।

Secured loan collateral — अगर loan के बदले property या कोई asset pledge था, वो bank के पास जा सकती है।

याद रखें — IFSC-linked bank branches directly RBI को default data report करती हैं। यह record permanently आपकी credit history में रहता है।

Section 80E — Tax का सबसे Underrated Benefit

Education loan repayment का एक बड़ा hidden benefit है जिसे ज़्यादातर graduates miss कर देते हैं।

Income Tax Act का Section 80E कहता है:

Education loan पर pay किए गए पूरे interest पर tax deduction मिलती है — कोई upper limit नहीं।

Rules:

Deduction 8 साल तक मिलती है — repayment start होने के साल से

Loan किसी recognised financial institution या approved charitable organisation से होना चाहिए

Family members या friends से लिए loan पर यह benefit नहीं मिलता

अगर parent co-borrower है और वो EMI pay कर रहे हैं — तो parent deduction claim करेगा

Example: अगर आप साल में ₹80,000 interest pay करते हैं, तो पूरे ₹80,000 tax से exempt हो जाते हैं। 30% tax bracket में यह ₹24,000 की direct savings है।

Prepayment — जब भी मौका मिले, Principal घटाओ

Signing bonus मिला? Freelance project से extra पैसे आए? Family support मिला?

तुरंत partial prepayment करें।

ज़्यादातर public sector banks education loan पर prepayment penalty नहीं लगाते — हालाँकि कुछ private lenders लगाते हैं, पहले confirm करें।

क्यों है prepayment इतना powerful:

Repayment के शुरुआती years में principal घटाने का effect compounding के कारण disproportionately बड़ा होता है

कम principal = कम interest = कम total loan cost

Tenure भी कम होती है

Practical Checklist — First EMI से पहले यह ज़रूर करें

✅ Moratorium end date confirm करें — bank से written communication लें

✅ Auto-debit setup करें EMI account पर — due date से 2 महीने पहले

✅ 2 months EMI buffer अपने account में हमेशा रखें

✅ Section 80E deduction के लिए bank से interest certificate लें हर साल

✅ CIBIL score regularly check करें — कोई error हो तो तुरंत dispute करें

✅ Loan account का IFSC code और account number safe जगह save करें

✅ अगर मुश्किल हो तो bank से पहले बात करें — ignore मत करें

निष्कर्ष — Loan Repayment को Manage करो, इसे Manage मत होने दो

Education loan repayment एक passive experience नहीं है — यह एक active financial responsibility है। जो graduates इस process को समझकर plan करते हैं — वही successfully और cleanly इससे बाहर निकलते हैं।

High salary वाले नहीं, informed borrowers जीतते हैं। Moratorium के दौरान interest pay करना, Section 80E का benefit लेना, prepayment का सही use करना — ये छोटी-छोटी smart moves हैं जो लाखों रुपये बचा सकती हैं। अपने education loan का IFSC-linked bank account regularly monitor करें और हर payment का record रखें — यही financial discipline आपकी credit health को आने वाले दशकों तक protect करेगी।